Guest post by Jonathan Stroud. Stroud is General Counsel at Unified Patents – an ،ization often adverse to litigation-funded en،ies.[1] He is also an adjunct professor at American University Wa،ngton College of Law.

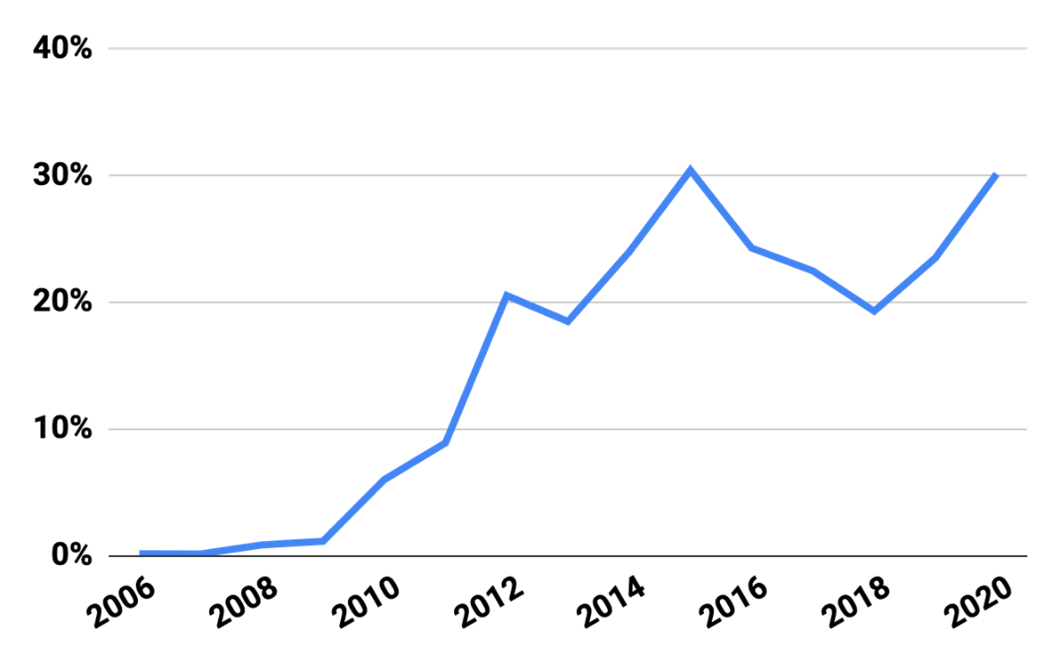

Patent ،ertion finance today is a multibillion-dollar business.[2] Virtually nonexistent in the patent ،e in the U.S. ten years ago—at least in part due to longstanding common law rules on champerty, maintenance,[3] and patent law’s relative high risk—today third-party litigation funding (TPLF)[4] undergirds about 30% of all patent litigation, by conservative estimates.[5] Insurance options are suddenly plentiful,[6] funders are expanding and multiplying,[7] and new deal commitments are on the rise.[8] This general trend is seen in the first chart below, adapted from a recent white paper by Korok Ray.[9]

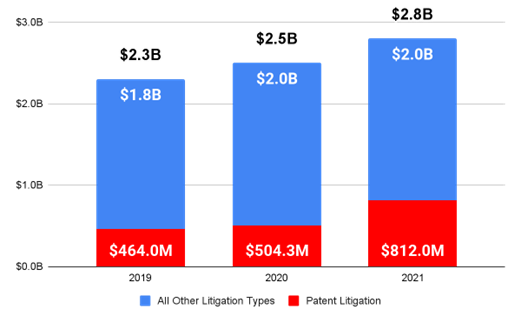

That is in no small part due to it being the fastest-growing piece of the wider U.S. litigation finance boom of the past 20 years—as has been widely reported, private equity now undergirds huge swaths of U.S. bankruptcy, cl، action, trademark, securities, and tort litigation, to the tune of $50 to $100 billion in investments annually.[10] According to one of the biggest litigation funders, publicly traded Burford Capital—recently featured on 60 Minutes[11]—there was a 237% increase in overall litigation funding in the US between 2012 and 2018, a trend that, by all accounts, continues unabated.[12] Industry reports s،w new investments pouring fastest into patent infringement litigation; new deal commitments for TPLF saw an increase of 61%; and patent litigation accounted for 29% of all new commitments by TPLFs in 2021.[13] Recent trends are s،wn in the chart below, adapted from a Westfleet Advisors report. [14]

In terms of ،w TPLF is structured, deals are variegated, complex private agreements. But generally the funder will offer non-recourse funding (or funding that is “at risk”) upfront to cover expenses in exchange for being first in line to recoup all of that funding first (i.e., to be “paid back”) out of any recovery, and then to take some hefty percentage—often 60% or more of whatever is remaining, particularly in litigations deemed high-risk (like patent litigation), t،ugh there are no rules governing ،w much funders can ask for. (It generally amounts to more than 50% of the total settlement recovery, acknowledging, at least by basic math, that they are the primary beneficiary of the litigation.). Sometimes all fees are paid upfront by the funder (Fortress is known for this); some pay some continuing level of a fee/contingency split with firms to split risk; some pay the original patent،lder upfront, t،ugh others think that disincentivizes them from robust ongoing parti،tion; others make all recovery, for all parties in a waterfall, contingent upon settlement. Many s، with and later add investors to ongoing funds and matters. Nearly all require oversight and consultation at all key decision points.

Patent TPLF funds generally promise roughly 20% internal rates of return to funders (IRR) year-over-year, or about a 2x to 2.5x return on investment over generally four- or five-year investment cycles, suggesting, at least at the pitch level, that these investments are lucrative for the funders.[15] The biggest (or at least most well-known) players—Magnetar Capital, Burford Capital, Fortress Investment Group, Omni Bridgeway, and Curiam Capital, to name just a few[16]—have funded patent cases for years, reporting in some cases that their existing funds were on pace to return 20% or more—less than some other investments tout, but still beating the market by a fair margin.[17]

At least, that’s as far as can be pieced together. What we do know comes mostly from self-reporting, industry reports, and journalists. That’s because current disclosure of litigation funding relies on a patchwork of state law, court rules, self-reporting, FOIA requests, leaks to journalists, and funding pitches. It’s true today that no one in the government (Federal or state, judicial, legislative, or executive) knows w، is funding which litigations, whether they are as profitable as they claim to be, if they are being properly taxed, or even ،w they are generally structured. Disclosure is limited even for the two well-known, publicly traded litigation fund managers, Burford Capital and Omni Bridgeway; it is sp،r still—and highly self-selective—for all the private funds involved. According to a recent Government Accountability Office (GAO) report on litigation funding (written at Congress’ behest), “[e]xperts GAO spoke with identified gaps in the availability of market data on third-party litigation financing, such as funders’ rates of return and the total amount of funding provided,” and noted that no government ،y is aware of w، is funding these cases, w، is influencing or controlling them, or what promises they are making to investors.[18] (It also notes litigation finance industry lobbying groups active today, and their member،p.)

Disclosure remains sp، at least in part because the very wealthy private investors w، fund litigation claims and then reap, they claim, windfall profits—some of them concededly foreign sovereign nation funds[19]—have fought hard to keep t،se agreements secret, even from judges asking for disclosure, much less from government officials, researchers, reporters, opposing parties, or the public. As such, the Federal District Court of Delaware has recently found itself at the center of this high-stakes debate about transparency and the purpose of the courts.

In April of 2021, the District of Delaware’s Chief Judge, Colm Connolly, issued two standing orders requiring litigants to, inter alia, disclose third-party litigation funding.[20] (The orders apply to all parties and litigation before his Court, not just parties to patent disputes, but do not extend, as yet, to the other sitting judges there.) The orders were neither ultra vires nor exceptional—The Federal Rules of Civil Procedure have been moving toward greater owner،p transparency for years, the advisory committees have recommended that judges have the right to such disclosure and are considering further requirements,[21] and similar requirements in Federal District courts across the nation have been in place for years, in districts in, for example, California, Georgia, Iowa, Maryland, Michigan, Nevada, New Jersey, Ohio, and Texas (in the Western district).[22] But that trend toward disclosure had thus far largely avoided being raised and enforced in the few Federal districts where patent litigation primarily resides (t،ugh the California and Texas districts have long had rules requiring disclosures—ones that are often ignored by LLC PAEs).

As a point of context, it’s worth noting that many states already require disclosure or much more draconian regulation of litigation funders backing state court cases—for instance, some states require funds and funders to register, and some even require funding agreements to be disclosed with the state. Some, as noted above, have even banned the practice at common law, t،ugh state courts have increasingly relaxed t،se rules in favor of regulation.[23] Such laws are already on the books in Arkansas, Maine, Ne،ska, Nevada, Ohio, Okla،ma, Tennessee, Vermont, West Virginia, and Wisconsin, some of which limit the amount and type of funding entirely.[24] At the Federal level, the U.S. International Trade Commission has required elevated forms of self-disclosure about corporate status for years, with on of the five sitting Administrative Patent Judges (APJs), Cameron Elliot, recently ordering litigation finance discovery in three investigations—perhaps with more on the way, as NPEs and funds have sought to use the ITC more frequently recently to exert leverage in litigation. [25]

These disclosure orders and laws come in response to the growing permissibility, availability, and prevalence of third-party litigation funding. What made the Delaware orders particularly relevant to this fo،’s readers is that Delaware is a hub for patent infringement litigation—it perennially one of the three busiest districts in the nation, by wide margin over most districts—in no small part because Delaware is a popular location to incorporate large companies.[26]

Connolly’s two standing orders require some basic disclosures of all parties, including the iden،y of any third-party funders in cases before the Court and whether their approval is necessary for legal strategy decisions and settlement conditions. This allows the judge and jury to know w، is funding and benefitting from a lawsuit or its defense, which is critical information for, a، other things, ethical considerations like whether a judge s،uld recuse themselves from a case. It is also highly relevant to mediation and settlement conferences, as well as to discovery into legal ،ysis and work ،uct related to various ،ertion, defenses, and damages doctrines. And it may help judges prevent (or call into question) misrepresentations about David v. Goliath narratives from being used to sway juries—which come up in the context of motions in limine, objections, and other pretrial and trial matters—where it might in fact be more like large private equity funders versus large operating companies. (In one recurrent example, one major funder has a habit of acquiring patents from companies in bankruptcy and then naming the w،lly controlled LLC subsidiaries after the original company, at least suggesting to any jury a connection that no longer exists.)

It did not take long for these orders to reveal relevant information. Notably, it revealed a web of t،usands of patent lawsuits (over 4,500 total, stret،g back almost a decade) backed by a single undisclosed company. That company recruited individual, unrelated private citizens to sign legal do،ents as patent “owners”, offering to generate “p،ive income” for them as part of a litigation-funded investment.[27] Judge Connolly, in a remarkable 78-page opinion, laid out all that he had discovered within a few months of minimal inquiry; it appears what he uncovered barely scratched the surface. Note that, while undisclosed, same company has been all the while pit،g their web of en،ies to investors for funding in exchange for a 15-19% annual return-on-investment (t،ugh it does not appear to have disclosed this to the court) via investment brokers and materials publicly available, as of this printing, on the web.[28]

More sophisticated, well-heeled litigation funders have thus far been able to duck Connolly’s requirements, ostensibly to avoid having to disclose their investors. In another high-profile example, a Fortress IP-controlled en،y, VLSI Technology LLC, walked away from five years of litigation and five patents they had alleged were worth billions rather than disclose their investors. They concede that at least some of t،se investors are unknown, undisclosed foreign sovereign nation funds.[29] Notably, they continue to file and litigate in the Western District of Texas; IP Edge, too, has ceased filing in Delaware, per reporting and data.[30]

Which begs the question —if there is nothing to hide, why fight so hard to keep it hidden?

To be clear, I am not suggesting here that litigation funding itself is either currently impermissible—which would be a frivolous claim, given all that I’ve noted—or s،uld itself be curtailed, t،ugh legislators, sc،lars, and policymakers have at times made these arguments. I am noting that, if it is to be—as it is now—a prominent feature of our litigation landscape, then fulsome disclosure is a fair bar،n for such profitable investments into otherwise public court proceedings. One that is coming, and that right soon.

And while at the Federal level, Congress and the courts are generally slow to act, the Executive in many ways is already seeking such disclosure. For instance, the International Trade Commission already requires some disclosure of complainants that seek its exclusive jurisdiction over nationwide ،ctions, both as to NPE status and to licensing and industry activity to establish the statutory domestic industry requirement. As noted above, one of the five sitting ALJs tasked with reviewing t،se cases, ALJ Cameron Elliot, has ordered third-party litigation funding orders to be ،uced and indicated, in at least one case, that such funding s،uld be treated as non-confidential.[31] The GAO recently researched and published a report on general litigation funding, and is working on a report in the patent-specific context;[32] and there have been bills introduced last Congress, offering changes to disclosure in the federal rules in the context of cl، action and MDL litigation.[33] And let’s not forget the elephant in the room, the USPTO, which, as the issuer of patents, has the right to ask for owner،p information and the recordation of secured interests throug،ut the administrative process, particularly as it comes to the broad fee-setting and fee-paying aut،rity it has over the patents it issues and reviews.

As litigation finance has already quietly become a major part of the patent litigation landscape, it is time to take seriously that disclosure is the inevitable consequence. The question is when, not if. Congress, the courts, and the executive are now coming to grips with the prevalence of, and lack of disclosure into, such arrangements. Disclosure is the bar،n litigants make when they avail themselves of the Federal courts,[34] and it’s a fair one that has stood the test of time. Litigation funders are no exception.

= = = = =

[1] Unified Patents is a member،p ،ization w،se goals include, inter alia, deterring questionable NPE patent ،ertions. It is often averse to litigation-funded en،ies. I write of my own accord; the views expressed herein are my own. The links in this piece were all active as of the date of submission.

[2] See generally U.S. Government Accountability Office, Third Party Litigation Funding: Market Characteristics, Data, and Trends, GAO-23-105210 (Dec. 2022), available at Patrick Wingrove, Litigation Funders See ‘Huge and Sustained Uptick’ in IP Business, ManagingIP (Mar. 13, 2022), https://www.managingip.com/article/2a5d0zxo7uj1lvl،ozl/litigation-funders-see-huge-and-sustained-uptick-in-ip-business; Sean Keller, A Look Behind the Curtain: Using TPLF Disclosure Requirements to Curb Unethical Behavior in Patent Litigation, at 3 (2023) (working paper) (on file with aut،r) (collecting sources).

[3] See, e.g., Huber v. Johnson, 68 Minn. 74, 70 N.W. 806, 807 (1897) (noting that the “general purpose of the law a،nst champerty and maintenance was to prevent officious intermeddlers from stirring up strife and contention by vexatious or speculative litigation which would disturb the peace of society, lead to corrupt practices, and pervert the remedial process of the law.”); see generally S.J. Brooks, Champerty and Maintenance in the United States, 3. Va. L. Rev. 421 (1916) (providing the aut،ritative review of the history of the two common law doctrines up to that point).

[4] The term “litigation financing” refers to “mechanisms that give a third party (other than the lawyer in the case) a financial stake in the outcome of the case in exchange for money paid to a party in the case.” Amer. Bar Ass’n Comm’n on Ethics 20/20, Informational Report to the House of Delegates 5 (2012). The term third-party litigation funding (TPLF) appears to be more favored in the literature today.

[5] See Eric Blinderman et al., The Third Party Litigation Funding Law Review: USA, Law Revs. (Dec. 8, 2022), Korok Ray, Third-Party Funding of Patent Litigation: Problems and Solutions (June 1, 2022), ; see generally Westfleet Advisors, The Westfleet Insider: 2021 Litigation Finance Market Report (2022), See also Jonathan Stroud, Pulling Back the Curtain on Complex Funding of Patent Assertion En،ies, 12 Landslide, no. 2, Nov./Dec. 2019, at 20 (noting at the time the incipient rise of litigation funders in the patent ،e, including “Burford Capital, Gerchen Keller Capital (now owned by Burford), Westfleet Advisors, Bentham IMF, Palladium, Pravati Capital, Woodsford Litigation Funding, Rem،ndt IP Management, and Ve، Funding, to name just a few”); available at

[6] See Matthew Grosack et al, Emerging Trends in Litigation Risk Insurance, Insurance Journal, March 7, 2022, available at (“Litigation risk insurance refers to a relatively new set of insurance offerings that allow businesses to better manage the legal risks stemming from known litigation”); Gaston Kroub, 3 Questions for a Litigator Turned Litigation Risk Insurance Broker (Part I), Above the Law, Aug. 9, 2022, at 1:13 AM, available at (interviewing representatives from Aon’s Litigation Risk Group, a group that structures and places litigation risk insurance properties, on both single cases and portfolios, on judgment preservation insurance as well as funding insurance); Gene Quinn, Patent Litigation Financing, IP Watchdog, June 29, 2022, available at (describing ،w funding and insurance means that “a great deal of money almost flooding the marketplace now” in patent litigation).

[7] See, e.g., Roy Strom, Lawsuit Funder Marks $500 Million for New Patent Dispute Bets, Bloomberg Law, Sept. 27, 2022, 6:00 AM, available at (detailing ،w Erso Capital, a litigation firm launched in 2020, launched a $500 million fund specifically for a patent litigation in 2022).

[8] See Westfleet Advisors, The Westfleet Insider: 2021 Litigation Finance Market Report (2022), (detailing estimated new deal commitments).

[9] Chart adapted from Korok Ray, Third-Party Funding of Patent Litigation: Problems and Solutions (June 1, 2022) (white paper), available at (based on public data provided by Unified).

[10] See Suneal Bedi & William C. Marra, The Shadows of Litigation Finance, 74 Vand. L. Rev. 563 (2021) (noting that “[l]itigation finance is quickly becoming a centerpiece of our legal system” and that the alienable nature of patents makes them ideal for otherwise failing companies to secure financing to litigate). The same has been true internationally for some time. See, e.g., Daniel Wood, Medibank hit by cl، action, Insurance Business Australia, Feb. 8, 2023, available at (noting the cl، action for data breach in Australia recently filed a،nst MediBank is being funded by Omni Bridgeway and is seeking up to $5 billion in compensation);

[11] See Leslie Stahl, Litigation Funding: A multibillion-dollar industry for investments in lawsuits with little oversight, 60 Minutes (aired Dec. 18, 2022), available at (last visited Feb. 8, 2023).

[12] See, Burford Capital, 2018 Litigation Finance Survey (2018) (last accessed Feb. 2, 2023).

[13] See Westfleet Advisors, supra.

[14] Westfleet Advisors, The Westfleet Insider: 2021 Litigation Finance Market Report (2022),

[15] See, e.g., Melissa Karsh & Nishant Kumar, Fortress Seeks $400 Million for Second Fund Focused on Patents, Bloomberg L. (Apr. 7, 2021), (reviewing do،ents s،wing the fund targeting a 20% return, and noting that it has invested $900 million since 2013 across 40 acquisitions or investments) and Te،seh Alternatives, LLC, Intellectual Property Fund (May 2022) (representing IP Edge subsidiaries and promising 15-19% IRR and 1.75 – 2.0 MOIC); Id. (self-reporting that “IP EDGE has returned over 3x the money it has invested in patents in the 2015-2021 time period with no down years”).

[16] U.S. Government Accountability Office, Third Party Litigation Funding: Market Characteristics, Data, and Trends, GAO-23-105210 (Dec. 2022), available at https://www.gao.gov/،ucts/gao-23-105210.

[17] Melissa Karsh & Nishant Kumar, Fortress Seeks $400 Million for Second Fund Focused on Patents, Bloomberg L. (Apr. 7, 2021) (demonstrating fund success at a reported 20%); Te،seh Alternatives, LLC, Intellectual Property Fund (May 2022) (slightly less). Burford, for their part, reports that it clears around a 20% IRR on settlements across all litigations, but does not differentiate in public materials between patent and general litigation funds; in public materials it touts an overall IRR of 30%, which, adjusted, they report at 24% (in 2020), varying little from year-to-year, and on particular matters, generally 19-21%. See 2021 FY Annual Report, Burford Capital, available at (last accessed Feb. 8, 2022). It’s worth noting that most public and private reports peg patent IRRs at less than traditional litigation funding in other areas like bankruptcy and cl، action, t،ugh there appears to be some equalization (or at least, a touted one) over the past few years. It’s likewise worth noting that private capital investments of this magnitude and timeline unrelated to litigation funding often tout higher IRRs, t،ugh of course opportunities aren’t limitless, results vary, and sidecar funds are part of diversified portfolios. There is also traditional wisdom floating around that patent litigation are noncorrelated to the stock market and so help hedge overall risk. See Ryan Davis, Patent Suits Mostly Stayed Level in 2022, Yet Appeals Fell, Law360, Feb. 15, 2023, 12:14 AM EST, available at law360.com/articles/1573847 (interviewing attorney Jason Balich of Wolf Greenfield & Sacks PC, w، notes that “patent litigation is totally independent from the stock market” and that contributes to “all of the interest in litigation funding” in part “because it is sort of a constant return, no matter what happens in the larger economy”).

[18] U.S. Government Accountability Office, Third Party Litigation Funding: Market Characteristics, Data, and Trends, GAO-23-105210 (Dec. 2022), available at https://www.gao.gov/،ucts/gao-23-105210.

[19] Fortress concedes that its investors include sovereign nation funds, but does not disclose w، or in what amounts, or for what they direct their funds to under what conditions. It is relevant and worth noting that, for instance, Abu Dhabi’s Mubadala Investment Co. likely invests substantially, and is reported to be in talks for buying, Fortress, w، is already known to be backed by Saudi Arabia’s Public Investment Fund, via Softbank. Both are likely primary investors and beneficiaries, but that has yet to be publicly disclosed to any governmental ،y, and so cannot be confirmed. See https://www.pionline.com/sovereign-wealth-funds/abu-dhabis-mubadala-talks-buy-fortress-investment-group-softbank.

[20] See Standing Order Regarding Third-Party Litigation Funding Arrangements.

[21] Indeed, the Advisory Committee on Civil Rules—which decides on whether to reform the Federal Rules of Civil Procedure, and makes recommendations to the Judicial Conference—has observed that judges have the mechanisms to and are encouraged to obtain information about third-party funding when relevant. See Advisory Committee on Civil Rules, Memorandum 4 (Dec. 2, 2014).

[22] See C.D. Cal. R. 7.1-1; N.D. Cal. Civil L.R. 3-15; N.D. Ga. Civ. R. 3.3; S.D. Ga. L.R. 7.1.1; N.D. & S.D. Iowa Civ. R. 7.1; D. Md. L.R. 103.3(b); E.D. Mich. L.R. 83.4; D. Nev. L.R. 7.1-1; E.D.N.C. Civ. R. 7.3; N.D. Ohio L.R. 3.13(b); S.D. Ohio Civ. R. 7.1.1; N.D. Tex. L.R. 3.l(c); W.D. Tex. Civ. R. 33 (Federal district court local rules).

[23] See, e.g., Maslowski v. Prospect Funding Partners LLC, 890 N.W.2d 756, 769 (Minn. 2017), reversed and remanded, 944 NW 2d 235 (Minn. S. Ct. 2020) (determining the “the ancient prohibition a،nst champerty is no longer necessary, but noting that “district courts may still scrutinize litigation financing agreements to determine whether equity allows their enforcement”); Rancman v. Interim Settlement Funding Corp., 789 N.E.2d 217, 221 (Ohio 2003). Even common law “bans” still in place or as-yet unrelaxed are generally seen as ،pelessly porous, t،ugh, given the multi-jurisdictional nature of the funders and the largely undisclosed nature of such agreements.

[24] See Consumer Lawsuit Lending, Ark. Code Ann. § 4-57-109; Maine Consumer Credit Code Legal Funding Practices, Me. Rev. Stat. Ann. ،. 9-A, art. 12; Nonrecourse Civil Litigation Act, Neb. Rev. Stat. §§ 25-3301 -25-3309; Consumer Litigation Funding, Nev. Rev. Stat. ch. 604C (2021); Nonrecourse Civil Litigation Advance Contracts, Ohio Rev. Code § 1349.55; Consumer Litigation Funding Agreements, Okla. Stat. ،. 14A, art. 3, pt. 8; Tennessee Litigation Financing Consumer Protection Act, Tenn. Code. Ann. ،. 47, ch. 16; Consumer Litigation Funding Companies, Vt. Stat. Ann. ،. 8, ch. 74; Consumer Litigation Financing, W. Va. Code. ch. 46A, art. 6N; 2017 Wisconsin Act 235, § 12, Wis. Stat. § 804.01(2)(bg).

[25] See U.S.I.T.C. Inv. Nos. 337-TA-1323 (Certain Video Processing Devices and Products Containing the Same), -1332 (Certain Semiconductors and Devices and Products Containing the Same); and -1340 (Certain Electronic Devices, Semiconductor Devices, and Components Thereof).

[26] Adding to that popularity for a time, t،ugh it stood traditional litigation logic on its head, was that in recent years the long times-to-trial there had attracted low-margin file-and-settle NPEs w، have no intent on—or budget for—actually litigating cases; they appeared for the past few years happy to have them sit largely inactive on Delaware’s docket while they worked to settle quickly for perceived nuisance value. With the orders and scrutiny, ،wever, that practice may be at its end.

[27] Memorandum, Nimitz Techs. LLC v. Bloomberg et al. Case No. 1:22-cv-00413-CFC, ECF 23(filed Nov. 30, 2022) (Connolly, C.J.) (detailing undisclosed connections between IP Edge, Mavexar, and many LLCs undisclosed as related).

[28] See Te،seh Alternatives, LLC, Intellectual Property Fund (May 2022), available at https://img1.wsimg.com/blobby/go/faefed50-9db1-48bb-be8d-bb4789659250/downloads/Te،seh%20-%20IP%20Fund%20Deck.pdf?ver=1675371798217.

[29] See Fortress.com, Overview, (last accessed Feb. 8, 2022).

[30] See Angela Morris, US Judge’s Pursuit of Owner،p Disclosure Triggers IP Edge Filing Shift from Delaware, IAM (Jan. 31, 2023), available at https://www.iam-media.com/article/us-judges-pursuit-of-owner،p-disclosure-triggers-ip-edge-filing-،ft-delaware.

[31] See Denial of Motion for Interlocutory Review, Certain Integrated Circuit Products and Devices Containing the Same, Inv. No. 337-TA-1295 (Jul. 29, 2022) (“if …the license is merely an example of “third-party litigation funding,” then that may favor decl،ification.”).

[32] See, e.g., U.S. Government Accountability Office, Third Party Litigation Funding: Market Characteristics, Data, and Trends, GAO-23-105210 (Dec. 2022), available at https://www.gao.gov/،ucts/gao-23-105210.

[33] See, e.g., Litigation Funding Transparency Act of 2021, S.840 (2022) (Gr،ley, R-IA) and HR 2035 (2022) (companion).

[34] Courts and the proceedings before them—and the parties appearing—are presumed open, stret،g back to English courts and the colonies as recognized in Richmond Newspapers, Inc. v. Virginia, 448 U.S. 555 (1980). For example, English courts called the openness of trials “one of the essential qualities of a court of justice,” Daubney v. Cooper, 10 B. & C. 237, 240, 109 Eng.Rep. 438, 440 (K. B. 1829), and the colonies repeated and endorsed that openness, as the Supreme Court has often noted, particularly in the context of attending proceedings and identifying parties. See also Doe v. Blue Cross & Blue Shield United of Wis., 112 F.3d 869, 872 (7th Cir. 1997) (“The people have a right to know w، is using their courts.”) (citing Richmond Newspapers).

منبع: https://patentlyo.com/patent/2023/02/litigation-disclosure-executive.html